Unlock Excellence in Taxation Services for Your Business and Personal Growth

For the first time in India, we have launched a concept of ‘Accounting with ease’. We provide Comprehensive Financial Solutions to business houses (Including Startups & SMEs) and individual taxpayers in India and around the globe. We stand as a primary platform committed to helping endless organizations.…‘Learn More’

- Expert Guidance

- Unified Service Contact

- Rapid Response

- Enhanced Transparency

- True Consultancy

- Dedicated Support

- Data Protection

- Economical Budget

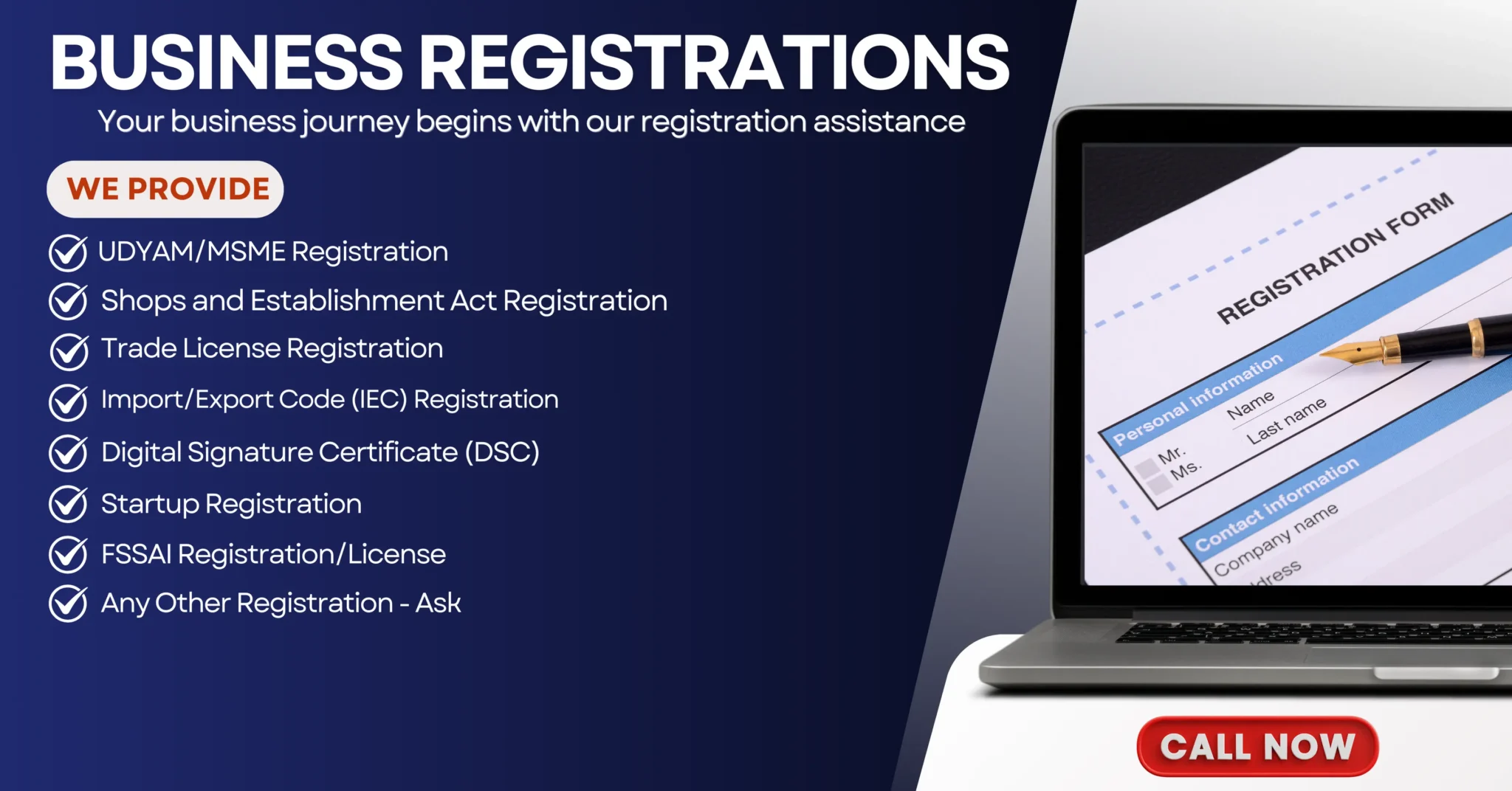

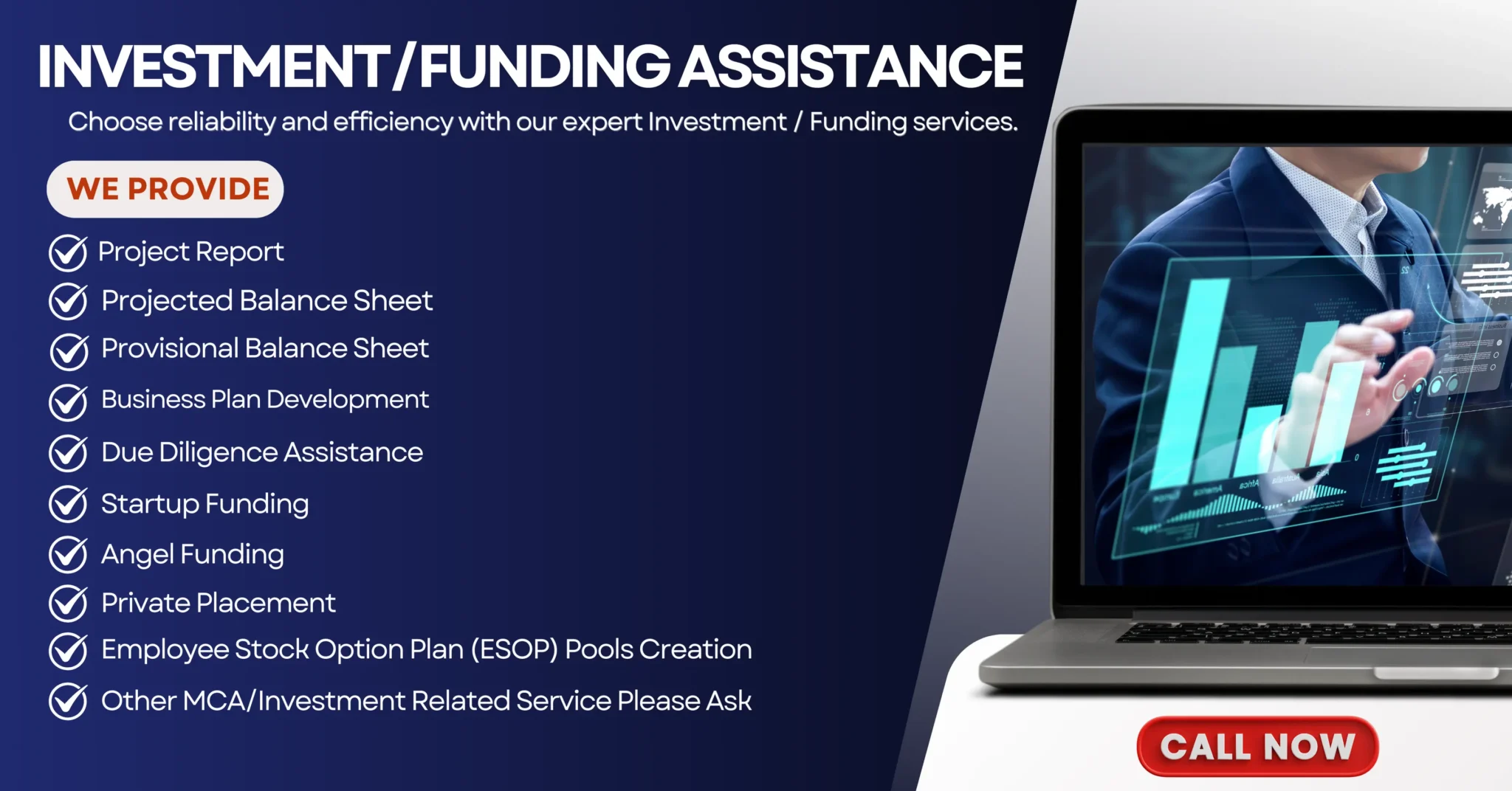

Our Services

Google Reviews

EXCELLENTTrustindex verifies that the original source of the review is Google. Good servicesPosted onTrustindex verifies that the original source of the review is Google. I had a fantastic experience working with Accteez for my all certificate needs. Their team of chartered accountants is highly knowledgeable and professional. They provided me with valuable insights and guidance, helping me navigate complex matters with ease.Posted onTrustindex verifies that the original source of the review is Google. Commendable servicePosted onTrustindex verifies that the original source of the review is Google. Acc Teez is Very good in service, friendly behaviour of staff. Response time is very quick. Special thanks to Himanshu, Tushar and team. Thank you so much for excellent service. Definitely recommend to everyone Thanks for all Team.Posted onTrustindex verifies that the original source of the review is Google. Superb ServicePosted onTrustindex verifies that the original source of the review is Google. Very nicePosted onTrustindex verifies that the original source of the review is Google. Best organization for resolving any concern related to GST and other services provided by them.

Our Partner

Our Client

Awards & Recognition

Blog

- Blog

What Are The Key Components Or Sections Included In A Typical Gst Return Form? WHAT ARE THE KEY COMPONENTS OR...

After Filing Under The Goods And Services Tax (Gst), Do We Need To Keep A Copy Of Every Invoice That...

What Are The Different Types Of Gst Returns And Their Respective Due Dates? Every registered person paying GST is required to furnish...

What Are The Key Components Or Sections Included In A Typical Gst Return Form? WHAT ARE THE KEY COMPONENTS OR SECTIONS INCLUDED IN A TYPICAL GST RETURN FORM? GST, or Goods and Services Tax, is a tax levied on the supply of goods and services in most countries around the world. It is a comprehensive indirect tax that has replaced multiple indirect taxes in many countries, including India. GST Return Form is a document containing details of all purchases, sales, output GST (on sales) and input tax credit (GST paid on purchases) to calculate an assesses GST liability for a particular tax period.. It helps businesses in India fulfill their Tax obligations under GST. GST forms are the various types of forms that taxpayers need to fill out and submit to the tax authorities to comply with GST regulations. These forms are used for registration, filing returns, claiming input tax credit, and other GST-related activities. Here are some common GST forms GST Return Forms: – GSTR-1: Monthly/Quarterly return for outward supplies – GSTR-3B: Summary return for monthly tax payment – GSTR-9: Annual return – GSTR-9C: Reconciliation statement and certification for annual return GSTR-1 is a monthly or quarterly return that should be filed by every registered GST taxpayer, except a few as given in further sections. It contains details of all outward supplies i.e sales. The return has a total of 13 sections, listed down as follows: Tables 1, 2 & 3: GSTIN, legal and trade names, and aggregate turnover in the previous year Table 4: Taxable outward supplies to registered persons (including UIN-holders) excluding zero-rated supplies and deemed exports Table 5: Taxable outward inter-state supplies to unregistered persons where the invoice value is more than Rs.2.5 lakh Table 6: Zero-rated supplies as well as deemed exports Table 7: Taxable supplies to unregistered persons other than the supplies covered in table 5 (net of debit notes and credit notes) Table 8: Outward supplies that are nil rated, exempted and non-GST in nature Table 9: Amendments to outward supplies that are taxable and reported in table 4, 5 & 6 of the earlier tax periods’ GSTR-1 return (including debit notes, credit notes, refund vouchers issued during the current period) Table 10: Debit note and credit note issued to unregistered person Table 11: Details of advances received or adjusted in the current tax period or amendments of the information reported in the earlier tax period. Table 12: Outward supplies summary based on HSN codes Table 13: Documents issued during the period. Table 14: For suppliers – Reporting ECO operators’ GSTIN-wise sales through e-commerce operators on which e-commerce operators are liable to collect TCS u/s 52 or liable to pay tax u/s 9(5) of the CGST Act Table 14A: For suppliers – Amendments to Table 14 Table 15: For e-commerce operators – Reporting both B2B and B2C, suppliers’ GSTIN-wise sales through e-commerce operators on which e-commerce operator must deposit TCS u/s 9(5) of the CGST Act Table 15A: For e-commerce operators – Table 15A I – Amendments to Table 15 for sales to GST registered persons (B2B) Table 15A II – Amendments to Table 15 for sales to unregistered persons (B2C) Form GSTR-3B is a simplified summary return and the purpose of the return is for taxpayers to declare their summary GST liabilities for a particular tax period and discharge these liabilities. A normal taxpayer is required to file Form GSTR-3B returns for every tax period GSTR-3B is divided into 7 sections. This article contains in detail each section/table of GSTR-3B and the details to be provided in it. Provide GSTIN(you can use your provisional id as your GSTIN if you do not have a GSTIN). Legal Name of the Registered Person[this field is auto-populated after entering GSTIN] Outward supplies and inward supplies on reverse charge i.e. Details where tax is payable by you These details are further broken down into the following Outward taxable supplies– Do not include supplies which are zero-rated, or have a nil rate of tax or are exempt from GST. These must be provided separately. Include only those supplies on which GST has been charged by you. Value of Taxable Supplies = Value of invoices + value of debit notes – value of credit notes + value of advances received for which invoices have not been issued in the same month – value of advances adjusted against invoices Details of advances as well as adjustment of advances against invoices are not required to be shown separately. Other outward supplies (nil rated, exempt)– include supplies which are exempt from GST or are nil rated. Nil-rated supplies are those for which the GST rate is nil. Or which have been kept exempt from GST. Inward supplies (liable to reverse charge)– provide details of purchases made by unregistered dealers on which reverse charge applies. In such cases, you have to prepare an invoice for yourself and pay the applicable GST rate of tax. Non-GST outward supplies– Non-GST outward supplies refer to the supplies of goods or services that are not subject to Goods and Services Tax (GST). These supplies are exempted from GST and do not attract any tax liability under the GST regime. Eligible ITC (A) ITC Available (whether in full or part) – This information must be broken down into ITC on: Import of goods, import of services, inward supplies on reverse charge (other than on import of goods and services reported above) inward supplies from your Input Service Distributor (ISD) basically your head office registered as an ISD under GST. all other ITC Our experts can help you calculate the amount of credit to be reported here. Input tax credit on the closing stock is not required to be reported here, as this input tax credit must be first reported by filling up TRAN-1 and TRAN-2 forms. (B) ITC Reversed As per rules 38, 42 and 43 of CGST Rules and sub-section (5) of section 17 (Prior to 5th July 2022, it was only as per rules 42 & 43 of CGST Rules) –

After Filing Under The Goods And Services Tax (Gst), Do We Need To Keep A Copy Of Every Invoice That We Create? This Subject is down to my alley. We are a tax Consulting and Accounting Company; I could tell you this: In the modern era of business landscape, the importance of keeping copies of invoices cannot be overstated. According to the Goods and Services Tax (GST) Act, which came into effect in India in 2017, orders businesses to maintain records of all transactions including invoices, receipts and other related documents. The GST Act instructs that at a minimum these records must be retained for six years at the end of the relevant financial year. This ensures that correct and complete records can be obtained for any audit, audit, or argument relating to GST compliance in transactions. Similarly, Indian Evidence Act, 1872, maintenance of records is not a business practice but also a legal requirement. Section 34 of the Act states that any document created for examination by any court shall be retained for a specified period. Depending on the nature of document and its importance to any current or potential claim, the length of time records should be retained may differ and it is mostly advisable to withhold some of the invoices preferably five to seven years. Companies should recognize the importance of record keeping and adopt the affidavits essential to use records in accordance with the Evidence Act and the GST Act. By doing so, they can ensure compliance, diminish risks, and control the power of successful financial documentation to strength their success in today’s active business environments. If you require assistance with GST, income tax, or any other financial and taxation services, feels free to contact Accteez Services India Private Limited. At AccTeez, we are committed to providing comprehensive GST, income tax, and accounting services to businesses of all sizes. With our team of experienced professionals and a client-centric approach, we strive to simplify complex financial processes and ensure compliance with tax regulations. Our team comprises highly skilled professionals with extensive knowledge and experience in taxation and accounting. We stay updated with the latest developments in tax laws to provide accurate and reliable services. As a trusted partner, AccTeez goes beyond providing accounting and tax services. We are committed to empowering businesses with knowledge and expertise, enabling them to navigate the complexities of record-keeping and stay compliant with the Evidence Act and GST Act. Email: consult@accteez.com Phone: +91 8860632015

What Are The Different Types Of Gst Returns And Their Respective Due Dates? Every registered person paying GST is required to furnish an electronic return every calendar month. A “Tax Return” is a document that showcases the income of a registered taxpayer. Such a document needs to be filed with the tax authorities in order to pay tax to the government. The tax to be paid by a registered dealer depends upon the income declared by such a person in the tax return filed with the tax authorities. There are various types of Goods and Services Tax (GST) returns in different countries, but I can provide you with general information about the types of GST returns and their respective due dates in India. GSTR – 1: Return for Outward Supplies GSTR-1 is a monthly return of outward supplies undertaken by a normal registered taxpayer under GST. In other words, this monthly return showcases the sales transactions of a business in a particular month. The due date for GSTR-1 is generally the 11th of the following month or the standard date for filing GSTR-1 is 10 days from the end of the month for which such a return is to be filed. GSTR – 2: Return for Inward Supplies GSTR-2 is a monthly return of inward supply of goods and services as agreed by the recipient of the goods and services. In other words, GSTR-2 contains details with regards to the purchases made by the recipient in a particular month. The information contained in GSTR-2 is auto-populated with the details contained in GSTR-2A. The process of making changes and filing GSTR-2 is required to be undertaken between 11th and 15th day of the succeeding month for which return is to be filed. GSTR – 2A: Read Only Document GSTR-2A is a read only document. This document gets auto-populated once the supplier uploads the details in GSTR-1. In other words, GSTR-2A enables the recipient to verify the details uploaded by the supplier in GSTR 1. Also the recipient could accept, reject, modify or keep the invoices pending using the said details. However, such changes are made by the recipient in GSTR 2. GSTR-2A is a read-only document used by the recipient to match the details uploaded by the supplier in GSTR-1. Thus, the recipient can accept, reject, modify or keep the invoices pending in case there is any mismatch. However, the recipient can make actual changes, if any, only in Form GSTR 2. This process of making changes and filing GSTR-2 is to be undertaken between 11th and 15th day of the month succeeding the month for which such a return is to be filed. GSTR – 3B: Summary of Inward and Outward Supplies This is a monthly return for regular taxpayers and requires the summary of outward supplies, input tax credit, and tax liability. It is a self-declaration of the taxpayer’s tax liability for the month and is filed even if there are no outward supplies. GSTR-3B is an interim return and needs to be filed along with the payment of taxes. The GSTR-3B must be submitted by the 20th of the month succeeding the tax period for which GST is filed. In case no transactions have been undertaken in a particular month, the registered person needs to file a NIL return for that period. GSTR – 4: Return For Composition Dealers This return is for composition scheme taxpayers who have opted for a simplified taxation scheme. It requires the details of outward supplies, inward supplies, and tax liability. GSTR-4 is filed quarterly, and it allows taxpayers to pay tax at a fixed rate without maintaining detailed records. GSTR – 5: Return For Non-Resident Taxable Persons This return is for non-resident taxpayers who are registered under GST and engage in business activities in India. It requires the details of inward and outward supplies made during the period. GSTR-5 is filed monthly and includes information about imports, exports, and any adjustments made to invoices. The details in GSTR 5 need to be filed within a time period that is earlier of: within 20 days after the end of the calendar month or within 7 days after the last date of validity of the registration GSTR – 6: Return For Input Service Distributors GSTR 6 is a monthly return that an Input Service Distributor files every calendar month. This return provides information of all the invoices on which credit has been received and is issued by an ISD. This means that it gives a summary of the total input tax credit available for distribution during a particular month. Thus, the details of the invoices that an ISD furnishes in form GSTR 6 are made available to every recipient of the credit. These details are visible to the recipient in part B of form GSTR 2A. GSTR-6 needs to be filed on the thirteenth day of the month succeeding the month for which tax is to be paid. GSTR – 7: Return For Taxpayers Deducting TDS This return is for taxpayers who are required to deduct tax at source (TDS) while making certain payments such as salaries, commissions, etc. It requires the details of TDS deducted and deposited GSTR-7A is an auto-generated form. The form gets generated once the deductor furnishes details in Form GSTR-7 on the common portal. If the details furnished by the deductor are accepted by the deductee, then a TDS certificate is made available to the deductee electronically. GSTR-7 is required to be filed by the deductor within 10 days after the end of the month in which the deduction was made GSTR 9 & 9C: Annual Return GSTR-9 is an annual return that needs to be filed by regular taxpayers. It requires the details of outward and inward supplies made during the financial year. It includes information about sales, purchases, input tax credit availed, and taxes paid. GSTR-9 is a consolidated summary of all the monthly/quarterly returns filed during the financial year. The due date for filing GSTR-9 is generally

Our Team

Error: No feed with the ID 1 found.

Please go to the Instagram Feed settings page to create a feed.